State of the global building industry

Steady growth in the Far East, Oceania and nations in the Persian Gulf.

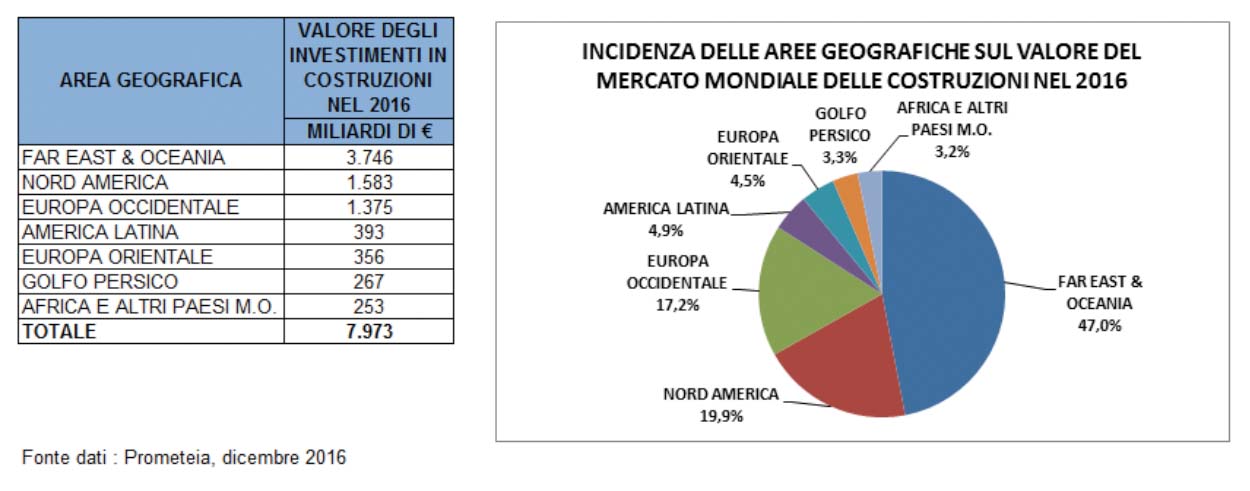

Investments in the building industry reached a figure of approximately 8,000 billion euros in 2016 corresponding to a rise of just over 2%. Last year the global building market grew more slowly than the world economy for which the International Monetary Fund estimates a growth of 3.1%.

FAR EAST & OCEANIA

This region has the world’s biggest building market with investments estimated at almost €3,750 billion and a 47% slice of the global construction market. Investments in construction per capita are less than €900, while in more mature markets like North America and Western Europe they are well over €3,000. This indicator highlights the future potential of Asia; indeed, there is plenty of room for a realignment between expenditure per capita in the various regions, which will move hand in hand with a reduction in the economic gap between emerging and mature markets.

Over recent years Asia has seen a partial slowdown in growth rates in the building industry, which, nevertheless, remain the highest worldwide in 2016. It is estimated that the market increased in value by 4.4% last year, rising perfectly in line with the overall growth in the economy. Investments are expected to increase by approximately 4% in 2017 and, in this case, the variation in the building industry should mirror that in the region’s GNP. The growth in the markets in the Far East and Oceania is not only due to such a colossus as China, but also other countries that have some of the world’s leading building markets. Indeed, the region also includes five of the world’s top construction markets: Japan, India, Indonesia, South Korea and Australia. The highest market increases are expected in India and Indonesia, while China will fall in line with the average figure for the region. Among the advanced economies, Australia and South Korea should show the best market trends, while the rise in investments in the building industry in Japan is expected to be more moderate, just like other mature economies.

NORTH AMERICA

The North American market is estimated to be worth almost €1,600 billion corresponding to 20% of the global construction industry. Canada and Mexico are stably in the list of the top 15 nations for investments in construction. It is estimated that investments in construction in North America increased by only 0.5% in 2016, a figure which is lower than the estimated 1.5% increase in the GNP. Modest growth in the North American building industry is entirely due to a slowdown in the non-residential and infrastructures sectors. Housing has, in fact, increased by over 4%. Last year there was relatively low growth in the USA and Mexico, while investments in construction in Canada dropped by over 2%. Estimates for 2017 show a clear improvement in the state of the North American building market. Investments in construction should, in fact, increase by over 3%, performing better than the region’s GNP, which is expected to rise by 2%. The positive outlook for the building industry is due to an expected revival in the non-residential and infrastructures markets. Growth in the housing sector is estimated at over 3%. This year’s rise in investments is estimated at approximately 4% in the United States, while the figure is expected to be around 2% in Mexico and Canada.

Investments in the building industry reached a figure of approximately 8,000 billion euros in 2016 corresponding to a rise of just over 2%. Last year the global building market grew more slowly than the world economy for which the International Monetary Fund estimates a growth of 3.1%.

WESTERN EUROPE

Western Europe is the world’s third most important building market with an estimated value of €1,375 billion and a 17% share of global investments. Germany, Great Britain, France and Italy are among the world’s top construction markets.

It is estimated that there was a just over 2% increase in investments in the region’s construction industry in 2016. This means the building industry has performed better than the economy, which grew by 1.6% last year. The most positive trend in all the various sections of the market came in the housing sector, which is estimated to have increased overall by between 3%-4%. In contrast the non-residential sector has grown least, suffering from the relatively low rise in GNP. All the main markets have seen a relatively moderate increase in building output, with the sole exception of Great Britain, where the building industry is expected to have stagnated.

Forecasts for 2017 indicate a moderate growth in construction estimated at 2%, which should be slightly higher in the residential sector. Among leading markets, growth in Germany, France and Italy should fall in line with the continental average, while investments are expected to contract by approximately 1% this year in Great Britain. Spain’s building industry is expected to perform best, where it is estimated that the market will increase by between 3%-4%. The positive trend in the Spanish building industry is mainly due to the residential sector, which had been hit hardest by the serious industrial recession in Iberian construction.

LATIN AMERICA

The region’s construction industry is estimated to be worth almost €400 billion, accounting for 5% of worldwide construction output. Slightly less than half of these investments were made in Brazil, which is the only country in the region among the world’s top construction markets.

The region’s economy and building industry performed worst on a worldwide scale in 2016. Indeed, the GNP is estimated as having contracted by approximately 2%, while the decline in the building industry is estimated at almost 4%. It is believed that the Latin American building industry lost 10% of its value during the three-year period from 2014-2016. The reason for this negative trend in GNP is the serious recession under way in Brazil, Venezuela and Argentina. The good trend in the market in certain countries in the region, including Colombia and Peru, could only slightly mitigate the overall recession in the Latin American building industry.

There is expected to be an improvement in the region’s economy this year with all markets coming out of recession, except for Venezuela’s. The overall increase in Latin America’s GNP is estimated at approximately 1%. Stronger growth estimated at 2.5% is expected in the building market. This estimate is based on meek signs of revival on the Brazilian building market, a relaunching of investments in Argentina, and the continuing expansion of other smaller markets in the region.

EASTERN EUROPE

Overall growth in this region was just over 1% in 2016, slowed down by the dip in Russia’s GNP (-0.8%), the region’s leading market. The region’s other two main economies, Poland and Turkey, grew by over 3% and the economic situation was also positive in central-eastern European countries.

Last year the region’s building industry went into recession: -1.7%. Alongside the crisis in the Russian building industry, the decline was also due to a drop in public investments in infrastructures, because of less access to EU funding. Following the 2016 recession, the region’s construction market saw a decline in its share of the global building industry; it is now estimated at 4.5% with investments estimated at approximately €360 billion.

This year Russia’s economy and building industry should come out of recession, recording growths of between 1%-2%. Overall, Eastern Europe’s GNP is expected to grow by approximately 2.5% and there is also expected to be a similar trend in the construction market.

PERSIAN GULF NATIONS

This region’s building market is estimated as being worth approximately €270 billion, corresponding to 3% of the global building output. It is estimated that investments in construction last year increased by 2.4% compared to 2015, showing similar growth to the regions GNP: +2.6%. The rise of the construction industry was negatively affected by the drop in the price of oil, which impacted on financing of public building projects. The countries most affected by low prices of crude was Saudi Arabia, while the GNP and construction industries of the Arab Emirates and Iran (thanks to the dropping of international sanctions) both performed positively. This year there is expected to be a slight increase in the rate of economic growth in the Gulf region, which should be helped along by an expected rise in the price of crude. Overall the building market is expected to improve notably, with an expected rise of approximately 5% in investments, the highest rate of growth in the construction industry worldwide. The Arab Emirates should show the best trend in building activities in the Gulf Region, partly due to projects linked with Expo 2020 in Dubai. The growth in the construction industry is expected to be more modest in Saudi Arabia, due to a slight drop in public spending for building. The construction market should show a positive trend in Iran: the country will be able to exploit the potential for growth of its housing and infrastructures markets.

AFRICA AND OTHER MIDDLE EASTERN COUNTRIES

The rate of economic growth in this region varied considerably last year: the GNP in North Africa and the middle eastern region was about 2.5%, while sub-Saharan Africa, negatively affected by the recession in Nigeria, only saw an increase of just 1.6%. Overall investments in construction in this region are estimated at €253 billion, corresponding to approximately a 3% share of the global building market. In this region, the market is mainly focused around infrastructures. The housing market has also been particularly dynamic over recent years, benefiting from the boost provided by urbanisation processes and the development of public building projects. The overall growth in the construction sector in 2016 is estimated at 2.3%. Egypt, Israel, Morocco and Tunisia are the nations where the building industry is most dynamic.

The economic situation in the region in 2017 should show signs of improving. Indeed, Nigeria is expected to come out of recession, which should allow sub-Saharan Africa’s GNP to grow by almost 3%. Economic growth in North Africa and the Middle East should be about 4.5%. The construction market should benefit from an improvement in the region’s macroeconomic situation and it is estimated that it could grow by over 4% in 2017. Of course, these forecasts depend on there being greater social and political stability in the region, which will encourage the influx of foreign investment required to develop the kind of major infrastructural projects Africa needs so badly.